")

Do you know that your credit score could have an impact on your financial life? Having a good credit score can open doors to better loan terms, lower interest rates, and even rental agreements. If your credit score isn’t where you’d like it to be, you have to believe me on this, the better your score, the easier you will find it to be approved for new loans or new lines of credit.

A higher credit score can also open the door to the lowest available interest rates when you borrow. With some dedication and smart strategies, you can improve your credit score in just six months. You need to hear this from me, A year ago, my credit score was 580—far from ideal. By following these steps, I boosted it to 720 in just six months. It wasn’t easy, but consistency and patience paid off. but these strategies that I am about to mention will guide long way to improve your credit score with simple steps.

In this article, you will be guided step by step on how to improve your credit score in not more than six months.

What is a Credit Score?

A credit score is a three-digit number that represents your creditworthiness. FICO scores range from 300 to 850. The higher the score, the more likely you are to get approved for loans and for better rates. The higher the score, the better your creditworthiness.

How Credit Scores are calculated

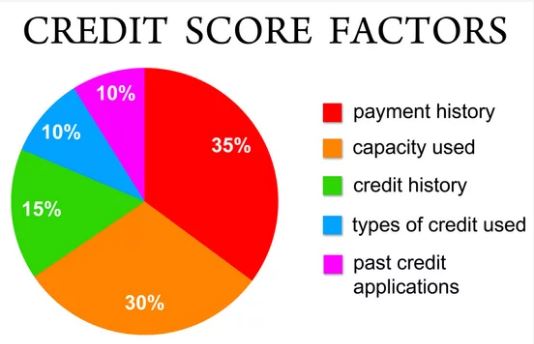

Credit scores are calculated based on five main factors: payment history, amounts owed, length of credit history, new credit, and credit mix. Each factor contributes differently to your overall score.

Five main factors are evaluated when calculating a credit score:

Payment history (35%)

Amounts owed (30%)

Length of credit history (15%)

Types of credit (10%)

New credit (10%)

Why Does a Good Credit Score Matter?

A good credit score is essential for unlocking financial opportunities and securing better terms in various aspects of life. It qualifies you for lower interest rates on loans and credit cards, saving you money over time. Lenders are more likely to approve your loan and credit card applications, and higher scores often lead to increased credit limits, offering more financial flexibility.

How to Improve Your Credit Score in 6 Months

Here are the steps to improve your credit score fast in less than 6 months.

Step 1: Check Your Credit Report

How to Obtain Your Credit Report

Before making any changes, you need to know where you stand. You can get a free copy of your credit report from each of the three major credit bureaus—Equifax, Experian, and TransUnion—once a year at AnnualCreditReport.com. you can also use this site to check your credit score Nairacompare.

Identifying Errors on Your Credit Report

Carefully review your credit reports for any errors or discrepancies. Common errors include incorrect personal information, accounts that don’t belong to you, and outdated account statuses.

Disputing Errors on Your Credit Report

If you find any errors, dispute them immediately. Each credit bureau has a process for disputing inaccuracies online or by mail. Correcting errors can quickly boost your credit score.

Step 2: Pay Your Bills on Time

Setting up Payment Reminders

Payment history is the most significant factor in your credit score. Set up payment reminders to ensure you never miss a due date. You can use calendar alerts or financial apps for this.

Automating Payments

Consider automating your payments to avoid the risk of forgetting. Most banks and credit card companies offer this service, which can give you peace of mind.

Impact of Late Payments on Your Credit Score

Late payments can severely impact your credit score. Even a single late payment can cause a significant drop, so it’s crucial to stay on top of your payment schedule.

Step 3: Reduce Your Debt

Creating a Debt Repayment Plan

Start by listing all your debts and create a repayment plan. Focus on paying off high-interest debts first while making minimum payments on others.

Using the Snowball vs. Avalanche Methods

The Snowball Method involves paying off the smallest debts first to build momentum, while the Avalanche Method focuses on paying off debts with the highest interest rates first. Choose the method that best suits your financial situation.

Avoiding New Debt

While paying off your existing debt, avoid taking on new debt. This can be challenging but is essential for improving your credit score.

Step 4: Keep Balances Low on Credit Cards

Understanding Credit Utilization Ratio

Your credit utilization ratio is the amount of credit you’re using compared to your credit limit. Keeping this ratio below 30% is crucial for a healthy credit score.

Strategies to Lower Credit Utilization

Pay down your credit card balances and try not to max out your cards. You can also request a credit limit increase to improve your utilization ratio.

Benefits of Low Credit Utilization

A low credit utilization ratio shows lenders that you manage credit responsibly, which can positively impact your credit score.

Step 5: Avoid Opening New Credit Accounts

Impact of Hard Inquiries on Credit Score

Each time you apply for new credit, a hard inquiry is made on your credit report, which can slightly lower your score. Avoid unnecessary credit applications during your credit improvement period.

Alternatives to Opening New Accounts

Instead of opening new accounts, focus on managing your existing ones responsibly. If you need more credit, consider a secured credit card or a credit-builder loan.

Step 6: Become an Authorized User

Benefits of Being an Authorized User

Becoming an authorized user on someone else’s account can help boost your credit score if the account has a positive history. You’ll benefit from their good credit habits.

How to Request Authorized User Status

Ask a family member or close friend with good credit if they can add you as an authorized user on their account. Ensure they have a strong payment history and low credit utilization.

Potential Risks and Considerations

While being an authorized user can help, it also comes with risks. If the primary account holder misses payments or carries a high balance, it could negatively affect your score.

Step 7: Diversify Your Credit Mix

Types of Credit Accounts

Having a mix of different types of credit—such as credit cards, installment loans, and mortgages—can positively impact your credit score.

Importance of a Diverse Credit Portfolio

Lenders like to see that you can manage different types of credit responsibly. Aim to have a healthy mix, but don’t open new accounts just for the sake of diversity.

Step 8: Keep Old Credit Accounts Open

Benefits of Long Credit History

The length of your credit history matters. Older accounts contribute to a longer average account age, which can help boost your score.

Managing Old Accounts Effectively

Keep your old accounts open and in good standing. Even if you don’t use them often, maintaining these accounts can positively impact your credit score.

Step 9: Regularly Monitor Your Credit

Tools and Services for Monitoring Credit

Use credit monitoring services to keep an eye on your credit report and score. Many banks and financial institutions offer free monitoring tools.

Importance of Staying Informed

Regularly checking your credit helps you spot errors early and understand how your actions affect your score. It also helps you stay on track with your improvement goals.

Common Mistakes to Avoid

Closing Credit Accounts

Do you want to improve your credit score? Closing credit accounts can reduce your available credit and increase your utilization ratio, negatively impacting your score.

Maxing Out Credit Cards

Maxing out your credit cards can significantly harm your credit score. Always aim to keep your balances low.

Applying for Multiple Credit Accounts at Once

Avoid applying for multiple credit accounts within a short period. Each application results in a hard inquiry, which can lower your score.

How to Maintain and Improve Your Credit Score

Long-Term Strategies for Good Credit Health

Once you’ve improved your credit score, maintain it by continuing to pay bills on time, keeping balances low, and monitoring your credit regularly.

Building Financial Discipline

Cultivate good financial habits, such as budgeting, saving, and managing debt effectively. Financial discipline is key to maintaining a good credit score.

Bottom Line

Improving your credit score in six months is achievable with dedication and the right strategies. Everybody will tell you this improving your credit score requires dedication, but the results are worth it. Better financial opportunities and peace of mind are just around the corner By checking your credit report, paying bills on time, reducing debt, and following the other steps outlined above, you can see significant improvements. Remember, maintaining a good credit score is a lifelong journey, so continue to practice good financial habits even after reaching your goal. Implementing these strategies will help you to improve your credit score.

Related Article

12 Top Financial Platforms in Nigeria to Follow for Expert Insights

Mastering Your Money: 7 Expert Tips to Build Wealth and Financial Freedom

11 Types of Marketing to Grow Your Business in 2024 (Complete Guide)

Some Frequently Asked Questions

How Quickly Can I See Improvements in My Credit Score?

You can start seeing improvements in as little as one to two months if you make significant changes, like paying down debt or correcting errors on your credit report.

What is the Best Way to Dispute an Error on My Credit Report?

Dispute errors by contacting the credit bureau that issued the report. Provide documentation to support your claim and follow up regularly until the error is corrected.

Can I Improve My Credit Score Without a Credit Card?

Yes, you can improve your credit score without a credit card by paying all bills on time, reducing debt, and being added as an authorized user on someone else’s credit card.

How Does Being an Authorized User Affect My Credit?

As an authorized user, the primary account holder’s good payment history can positively impact your credit score. However, if they miss payments or carry high balances, it can negatively affect your score.

What Should I Do if I Can’t Pay My Bills on Time?

If you can’t pay your bills on time, contact your creditors to discuss your options. They may offer payment plans or hardship programs to help you manage your payments.

{kind=link}